Behavioural finance research makes it clear that we are all victims of our own biases. Dan Kahneman, who is likely the world’s leading researcher on bias, has this depressing conclusion as it concerns bias: “The odd thing is that educating people doesn’t seem to be enough, because we find that educated people are not less polarized than non-educated people in their politics and their biases.”

What are the consequences of this for financial planning? Should we be concerned that we are helping a client to make decisions, but are stuck in a path carved out by our own biases? How can I know if I am making the right recommendation when a client asks me about using a TFSA first or an RRSP first, or if saving is even the right thing for that client?

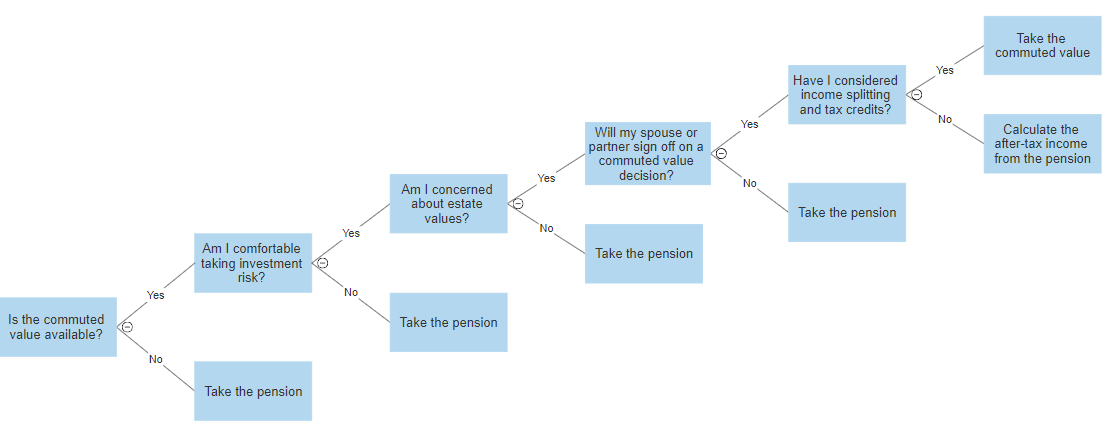

I have a suggestion for one possible way to address this. Create a tool like the decision-tree below for helping a client to make decisions that commonly come across your desk. By removing your own decision-making from the outcome, you might be able to reduce bias.

How can we be sure that we don’t apply our bias in building the decision-making tool? By back-testing it, we should be able to identify and remove our own bias. Run the last 10 or 12 clients you’ve seen with this question through this decision-tree. If all of them end up with the same outcome, there is likely some bias in this tool.

Consider a tool like this for common financial planning decisions:

- RRSP or TFSA

- Corporate investing or personal investing

- Buy or rent a place to live

- Use the HBP to avoid CMHC fees

- Permanent or term insurance

- Incorporate a business

For each of these, I would suggest a decision-tree tool would help to come to better client outcomes. I built the tool above using the free resources at www.smartdraw.com, but you can use similar tools in the Microsoft Office or G Suite of tools.